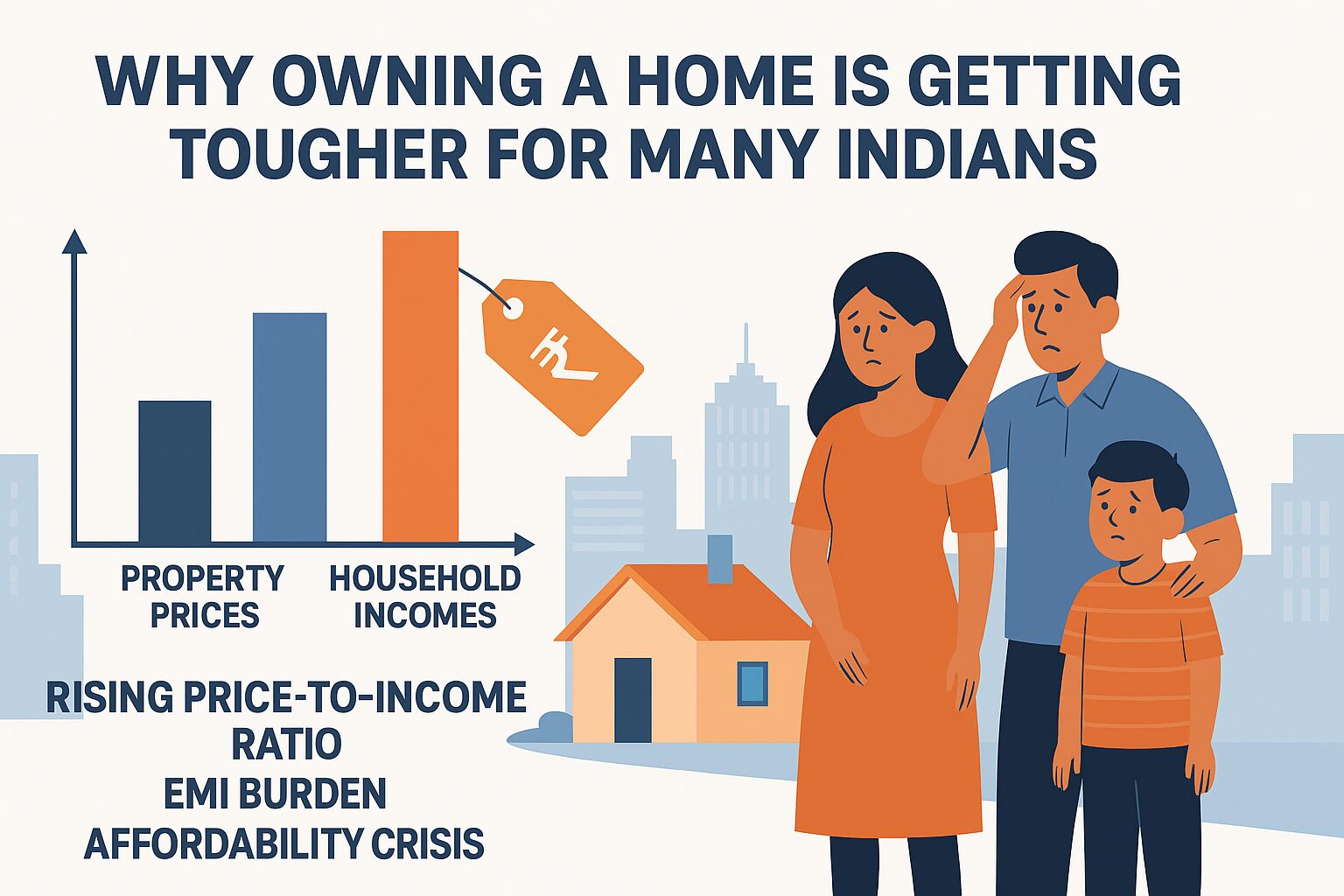

Homeownership Crisis India

In a country where homeownership has long symbolized stability and social status, the dream of buying a home is becoming increasingly elusive for many Indians. Despite government schemes and rising urban development, housing affordability has deteriorated over the past decade due to the growing gap between property prices and income levels.

Let’s explore what’s making homeownership more difficult—and what it means for aspiring buyers across the country.

📈 Property Price Growth vs Income Growth

Over the last 10–15 years, property prices in many Indian metros have risen at a much faster rate than household incomes. While salaries have increased modestly (around 5–7% annually), real estate prices have surged at 10–15% in many urban centers.

| Year | Avg Income Growth | Avg Property Price Growth |

|---|---|---|

| 2010–2020 | ~6% annually | ~11% annually |

| 2020–2024 | ~4–5% (post-pandemic recovery) | ~10–12% (especially in Tier-1 cities) |

This disparity means that what was once affordable with 5–6 years of savings may now take 10+ years of disciplined financial planning.

📊 Price-to-Income Ratio: A Measure of Affordability

The Price-to-Income (P/I) Ratio is a globally accepted metric that compares the average cost of a home to the average household income. A lower ratio means better affordability.

Here’s how Indian cities fare (as of 2024 estimates):

| City | Avg Property Price (INR) | Avg Annual Income (INR) | P/I Ratio |

|---|---|---|---|

| Mumbai | ₹1.8 Cr | ₹12 lakh | 15.0 |

| Delhi NCR | ₹1.2 Cr | ₹10 lakh | 12.0 |

| Bengaluru | ₹95 lakh | ₹11 lakh | 8.6 |

| Chennai | ₹85 lakh | ₹9 lakh | 9.4 |

| Hyderabad | ₹90 lakh | ₹9.5 lakh | 9.5 |

💡 Global affordability standard: A P/I ratio below 5 is considered affordable. As the numbers show, most Indian cities exceed this benchmark significantly, making homeownership out of reach for the middle class.

🏦 Rising Loan EMIs and Interest Rates

Even though home loan interest rates have come down since the peak of the pandemic, property prices have increased, leading to higher EMIs. A ₹1 crore property that required a ₹60 lakh loan in 2015 now requires a ₹90 lakh loan in 2024, even at the same interest rate.

This also leads to:

- Longer loan tenures (20–30 years)

- Higher monthly burden on disposable income

- Increased financial stress for young families

🏘️ Urban Migration vs Supply Mismatch

Rapid urbanization has driven demand in Tier-1 and Tier-2 cities, but housing supply hasn’t kept pace with population growth. Affordable housing remains in short supply due to:

- Limited land in urban cores

- Escalating construction costs

- Focus of developers on luxury and mid-segment markets

📉 Stagnant Incomes in Lower & Middle Segments

While upper-income professionals have seen decent wage growth, blue-collar and lower-middle-class workers have experienced stagnant earnings, worsening inequality in housing access.

- Informal sector still comprises ~80% of India’s workforce

- Lack of access to formal credit restricts housing options

- Many households rely on rental markets or shared housing

🔍 Final Thoughts: Bridging the Affordability Gap

The dream of owning a home is still alive, but economic realities are redefining the timeline and strategies needed to achieve it. Government policies like PMAY and subsidy schemes help, but structural reforms are essential.

🧠 Takeaway: Aspiring homebuyers must plan earlier, consider plotted developments or suburban areas, and stay financially disciplined to navigate the affordability crunch.

🏁 Are You Ready to Buy?

- Do you know your city’s price-to-income ratio?

- Are your savings and EMIs aligned with your housing goals?

- Have you considered investing in emerging micro-markets?